Germany has triggered a near-panic flight from southern European debt markets by warning that there will be no EU bail-outs, even though it fears the region's economic crisis has turned dangerous and could prove "fatal" for the entire eurozone.

The yield on 10-year Greek bonds blasted upwards by over 40 basis points to 7.15pc in a day of wild trading. Spreads over German Bunds reached almost four percentage points, by far the highest since Greece joined the euro, and close to levels that risk a self-feeding spiral. Contagion hit Portuguese, Spanish, Irish, and Italian bonds.

George Papandreou, the Greek premier, said in Davos that his country had been singled out as the weak link in a "attack on the eurozone" by speculators and political foes. "We are being targeted, particularly by those with an ulterior motive."

Marc Ostwald, from Monument Securities, said the botched bond issue of €8bn (£6.9bn) of Greek debt earlier this week has made matters worse. Many of the investors were "hot money" funds that bought on rumours that China was emerging as a buyer, offering them a chance for quick profit. When the China story was denied by Beijing and Athens, these funds rushed for the exit.

However, a key trigger yesterday was testimony in Germany's parliament by economy minister Rainer Brüderle, who said there would be "no bail-outs" for struggling debtors and no move to a "European economic government".

"A few European nations are exhibiting dangerous weaknesses. That could have fatal consequences for all countries in the eurozone," he said. Despite the warning, he said each country must solve its own problems.

"Germany is not in a mood to be the deep pocket for what they consider profligate, southern neighbours," said hedge fund doyen George Soros.

Mr Brüderle's hard line contradicts a report in Le Monde that Franco-German officials are discussing a rescue for Greece in order to keep the International Monetary Fund at bay.

The paper cited a source saying that EMU partners were ready to "help" Greece. "It is a question of credibility for the eurozone. The IMF might want to impose monetary conditions."

Le Monde's story was shot down by Berlin and Paris, but there is little doubt that certain officials have been trying to build momentum for a rescue. It is clear that the EU family is split on the issue. Jean-Claude Juncker, head of the Eurogroup of finance ministers, backs "assistance", with support of EU integrationists hoping to nudge the EU towards full fiscal union.

This is fiercely opposed by Berlin, and the German-led bloc at the European Central Bank. There are reports that Berlin is deliberately bringing the crisis to a head, hoping to lance the boil early and force the Club Med states to reform before it is too late. If so, this is a risky strategy. German banks have huge exposure to Greek, Spanish, and Portuguese debt.

Hans Redeker, currency chief at BNP Paribas, said Greece will face "great trouble" if it has to pay 7pc rates for long. Athens must raise €53bn this year, mostly in the first half. It has a been relying on cheap short-term debt to fund the budget deficit of 13pc of GDP, but this raises "roll-over risk".

Tim Congdon, from International Monetary Research, said the danger is that wealthy Greeks may shift money to bank accounts abroad if they lose confidence (akin to Mexico's Tequila Crisis in 1994-1995). This would set off a banking crisis and become self-fulfilling.

Greece has been financing current account deficits – 15pc of GDP in 2008 – through its banks, which have built up €110bn foreign liabilities. "If foreign creditors want their money back, defaults and/or a macroeconomic catastrophe appear inevitable," Mr Congdon said.

Adding to worries, Moody's has issued an alert on Portugal's "adverse debt dynamics", saying Lisbon needs a "credible plan" to reduce a structural deficit stuck at 7pc of GDP rather than "one-off measures".

The deeper concern is Spain, where youth unemployment has reached 44pc and the housing bust has a long way to run. Nouriel Roubini – the economist known as 'Dr Doom' – said Spain is too big to contain. "If Greece goes under that's a problem for the eurozone. If Spain goes under it's a disaster," he said.

Jose Luis Zapatero, Spain's premier, replied wearily: "Spanish public debt (52pc of GDP) is 20pc lower than Europe's average; our treasury spends 5pc of revenues on debt costs, less than France and Germany. Nobody is going to leave the euro," he said.

Friday, January 29, 2010

Wednesday, January 27, 2010

The children of illegal aliens (anchor babies) have bankrupted the state of California

In 2009, San Bernardino County spent $64 million providing welfare benefits to U.S.-born children of illegal aliens.

According to county records, during a typical month, close to 15,000 offspring of illegal aliens received either welfare payments or food stamps in 2009. Over 11,000 of those children received both forms of assistance.

Assemblyman Steve Knight, R-Palmdale, told the San Bernardino Sun: "This is a huge burden on our state. Obviously, these kids are U.S. citizens and that's fine. But when you look at it, these parents should have never been here in the first place."

Raymond Herrera, founder and president of We The People California's Crusader, said: "The American people are fed up with illegal aliens depleting our tax dollars by overrunning our schools, our hospitals and our welfare system."

While $64 million more than the county can afford particularly during the current deep recession, it is but a drop in the bucket, when you consider what the entire state of California is paying-out to ‘anchor babies’ and their illegal alien parents.

In August 2009, Los Angeles County Supervisor Michael Antonovich made public the staggering amount which the taxpayers spend on illegal aliens, living in L.A. County. Last June alone, the county paid out $48 million to the children of illegal aliens, an increase of $10 million over June 2007.

$26 million of that total came in the form of food stamps, while another $22 million was given to the illegal alien families in welfare checks.

Assuming that June was a typical month for 2009, Los Angeles County spent nearly $600 million on those two programs last year alone. That is in addition to the more than $1 billion that the county spends annually on the medical treatment, education, emergency services, and incarceration of illegal aliens.

These figures explain why not only L.A. County, but the entire state of California are now in financial ruin. Supervisor Michael Antonovich told reporters that illegal aliens continue to have a “catastrophic impact on Los Angeles County taxpayers.”

In 2003, the American Southwest saw 77 hospitals enter bankruptcy due to unpaid medical bills incurred by illegal aliens. A staggering 84 hospitals in California alone, have been forced to close their doors because of the growing crisis. Hospitals which manage to remain open, pass the unpaid costs onto the rest of us, which translates into more out-of-pocket expenses and higher insurance premiums for Americans.

With rising unemployment, huge trade deficits due to the loss of our manufacturing base, and a soaring national debt, we simply cannot afford to pay the bills for this nation’s illegal alien population. We can no longer accept elected representatives who choose to better represent a foreign national population, rather than those of us who actually pay their salaries.

Illegal immigration is slowly but surely destroying this nation.

According to county records, during a typical month, close to 15,000 offspring of illegal aliens received either welfare payments or food stamps in 2009. Over 11,000 of those children received both forms of assistance.

Assemblyman Steve Knight, R-Palmdale, told the San Bernardino Sun: "This is a huge burden on our state. Obviously, these kids are U.S. citizens and that's fine. But when you look at it, these parents should have never been here in the first place."

Raymond Herrera, founder and president of We The People California's Crusader, said: "The American people are fed up with illegal aliens depleting our tax dollars by overrunning our schools, our hospitals and our welfare system."

While $64 million more than the county can afford particularly during the current deep recession, it is but a drop in the bucket, when you consider what the entire state of California is paying-out to ‘anchor babies’ and their illegal alien parents.

In August 2009, Los Angeles County Supervisor Michael Antonovich made public the staggering amount which the taxpayers spend on illegal aliens, living in L.A. County. Last June alone, the county paid out $48 million to the children of illegal aliens, an increase of $10 million over June 2007.

$26 million of that total came in the form of food stamps, while another $22 million was given to the illegal alien families in welfare checks.

Assuming that June was a typical month for 2009, Los Angeles County spent nearly $600 million on those two programs last year alone. That is in addition to the more than $1 billion that the county spends annually on the medical treatment, education, emergency services, and incarceration of illegal aliens.

These figures explain why not only L.A. County, but the entire state of California are now in financial ruin. Supervisor Michael Antonovich told reporters that illegal aliens continue to have a “catastrophic impact on Los Angeles County taxpayers.”

In 2003, the American Southwest saw 77 hospitals enter bankruptcy due to unpaid medical bills incurred by illegal aliens. A staggering 84 hospitals in California alone, have been forced to close their doors because of the growing crisis. Hospitals which manage to remain open, pass the unpaid costs onto the rest of us, which translates into more out-of-pocket expenses and higher insurance premiums for Americans.

With rising unemployment, huge trade deficits due to the loss of our manufacturing base, and a soaring national debt, we simply cannot afford to pay the bills for this nation’s illegal alien population. We can no longer accept elected representatives who choose to better represent a foreign national population, rather than those of us who actually pay their salaries.

Illegal immigration is slowly but surely destroying this nation.

Tuesday, January 26, 2010

Economic Black Hole: 20 Reasons Why The U.S. Economy Is Dying And Is Simply Not Going To Recover

Economic Black Hole: 20 Reasons Why The U.S. Economy Is Dying And Is Simply Not Going To Recover

Even though the U.S. financial system nearly experienced a total meltdown in late 2008, the truth is that most Americans simply have no idea what is happening to the U.S. economy. Most people seem to think that the nasty little recession that we have just been through is almost over and that we will be experiencing another time of economic growth and prosperity very shortly. But this time around that is not the case. The reality is that we are being sucked into an economic black hole from which the U.S. economy will never fully recover.

The problem is debt. Collectively, the U.S. government, the state governments, corporate America and American consumers have accumulated the biggest mountain of debt in the history of the world. Our massive debt binge has financed our tremendous growth and prosperity over the last couple of decades, but now the day of reckoning is here.

And it is going to be painful.

The following are 20 reasons why the U.S. economy is dying and is simply not going to recover....

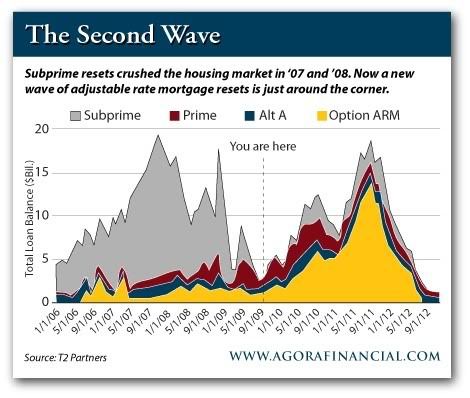

#1) Do you remember that massive wave of subprime mortgages that defaulted in 2007 and 2008 and caused the biggest financial crisis since the Great Depression? Well, the "second wave" of mortgage defaults in on the way and there is simply no way that we are going to be able to avoid it. A huge mountain of mortgages is going to reset starting in 2010, and once those mortgage payments go up there are once again going to be millons of people who simply cannot pay their mortgages. The chart below reveals just how bad the second wave of adjustable rate mortgages is likely to be over the next several years....

#2) The Federal Housing Administration has announced plans to increase the amount of up-front cash paid by new borrowers and to require higher down payments from those with the poorest credit. The Federal Housing Administration currently backs about 30 percent of all new home loans and about 20 percent of all new home refinancing loans. Tighter standards are going to mean that less people will qualify for loans. Less qualifiers means that there will be less buyers for homes. Less buyers means that home prices are going to drop even more.

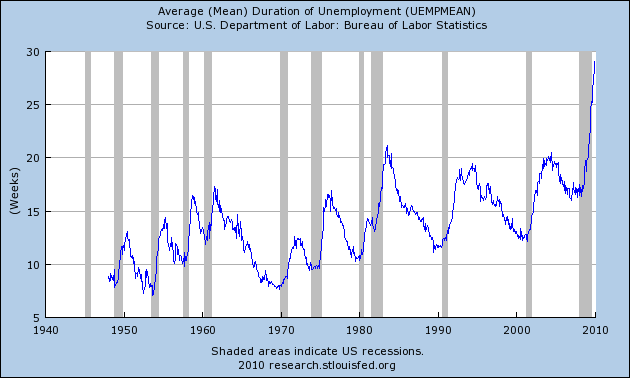

#3) It is getting really hard to find a job in the United States. A total of 6,130,000 U.S. workers had been unemployed for 27 weeks or more in December 2009. That was the most ever since the U.S. government started keeping track of this statistic in 1948. In fact, it is more than double the 2,612,000 U.S. workers who were unemployed for a similar length of time in December 2008. The reality is that once Americans lose their jobs they are increasingly finding it difficult to find new ones. Just check out the chart below....

#4) In December, there were also 929,000 "discouraged" workers who are not counted as part of the labor force because they have "given up" looking for work. That is the most since the U.S. government first started keeping track of discouraged workers in 1949. Many Americans have simply given up and are now chronically unemployed.

#5) Some areas of the U.S. are already virtually in a state of depression. The mayor of Detroit estimates that the real unemployment rate in his city is now somewhere around 50 percent.

#6) For decades, our leaders in Washington pushed us towards "a global economy" and told us it would be so good for us. But there is a flip side. Now workers in the U.S. must compete with workers all over the world, and our greedy corporations are free to pursue the cheapest labor available anywhere on the globe. Millions of jobs have already been shipped out of the United States, and Princeton University economist Alan S. Blinder estimates that 22% to 29% of all current U.S. jobs will be offshorable within two decades. The days when blue collar workers could live the American Dream are gone and they are not going to come back.

#7) During the 2001 recession, the U.S. economy lost 2% of its jobs and it took four years to get them back. This time around the U.S. economy has lost more than 5% of its jobs and there is no sign that the bleeding of jobs is going to stop any time soon.

#8) All of this unemployment is putting severe stress on state unemployment funds. At this point, 25 state unemployment insurance funds have gone broke and the Department of Labor estimates that 15 more state unemployment funds will likely go broke within two years and will need massive loans from the federal government just to keep going.

#9) 37 million Americans now receive food stamps, and the program is expanding at a pace of about 20,000 people a day. The United States of America is very quickly becoming a socialist welfare state.

#10) The number of Americans who are going broke is staggering. 1.41 million Americans filed for personal bankruptcy in 2009 - a 32 percent increase over 2008.

#11) For decades, the fact that the U.S. dollar was the reserve currency of the world gave the U.S. financial system an unusual degree of stability. But all of that is changing. Foreign countries are increasingly turning away from the dollar to other currencies. For example, Russia’s central bank announced on Wednesday that it had started buying Canadian dollars in a bid to diversify its foreign exchange reserves.

#12) The recent economic downturn has left some localities totally bankrupt. For instance, Jefferson County, Alabama is on the brink of what would be the largest government bankruptcy in the history of the United States - surpassing the 1994 filing by Southern California's Orange County.

#13) The U.S. is facing a pension crisis of unprecedented magnitude. Virtually all pension funds in the United States, both private and public, are massively underfunded. With millions of Baby Boomers getting ready to retire, there is simply no way on earth that all of these obligations can be met. Robert Novy-Marx of the University of Chicago and Joshua D. Rauh of Northwestern's Kellogg School of Management recently calculated the collective unfunded pension liability for all 50 U.S. states for Forbes magazine. So what was the total? 3.2 trillion dollars.

#14) Social Security and Medicare expenses are wildly out of control. Once again, with millions of Baby Boomers now at retirement age there is simply going to be no way to pay all of these retirees what they are owed.

#15) So will the U.S. government come to the rescue? The U.S. has allowed the total federal debt to balloon by 50% since 2006 to $12.3 trillion. The chart below is a bit outdated, but it does show the reckless expansion of U.S. government debt over the past several decades. To get an idea of where we are now, just add at least 3 trillion dollars on to the top of the chart....

#16) So has the U.S. government learned anything from these mistakes? No. In fact, Senate Democrats on Wednesday proposed allowing the federal government to borrow an additional $2 trillion to pay its bills, a record increase that would allow the U.S. national debt to reach approximately $14.3 trillion.

#17) It is going to become even harder for the U.S. government to pay the bills now that tax receipts are falling through the floor. U.S. corporate income tax receipts were down 55% in the year that ended on September 30th, 2009.

#18) So where will the U.S. government get the money? From the Federal Reserve of course. The Federal Reserve bought approximately 80 percent of all U.S. Treasury securities issued in 2009. In other words, the U.S. government is now being financed by a massive Ponzi scheme.

#19) The reckless expansion of the money supply by the U.S. government and the Federal Reserve is going to end up destroying the U.S. dollar and the value of the remaining collective net worth of all Americans. The more dollars there are, the less each individual dollar is worth. In essence, inflation is like a hidden tax on each dollar that you own. When they flood the economy with money, the value of the money you have in your bank accounts goes down. The chart below shows the growth of the U.S. money supply. Pay particular attention to the very end of the chart which shows what has been happening lately. What do you think this is going to do to the value of the U.S. dollar?....

#20) When a nation practices evil, there is no way that it is going to be blessed in the long run. The truth is that we have become a nation that is dripping with corruption and wickedness from the top to the bottom. Unless this fundamentally changes, not even the most perfect economic policies in the world are going to do us any good. In the end, you always reap what you sow. The day of reckoning for the U.S. economy is here and it is not going to be pleasant.

Even though the U.S. financial system nearly experienced a total meltdown in late 2008, the truth is that most Americans simply have no idea what is happening to the U.S. economy. Most people seem to think that the nasty little recession that we have just been through is almost over and that we will be experiencing another time of economic growth and prosperity very shortly. But this time around that is not the case. The reality is that we are being sucked into an economic black hole from which the U.S. economy will never fully recover.

The problem is debt. Collectively, the U.S. government, the state governments, corporate America and American consumers have accumulated the biggest mountain of debt in the history of the world. Our massive debt binge has financed our tremendous growth and prosperity over the last couple of decades, but now the day of reckoning is here.

And it is going to be painful.

The following are 20 reasons why the U.S. economy is dying and is simply not going to recover....

#1) Do you remember that massive wave of subprime mortgages that defaulted in 2007 and 2008 and caused the biggest financial crisis since the Great Depression? Well, the "second wave" of mortgage defaults in on the way and there is simply no way that we are going to be able to avoid it. A huge mountain of mortgages is going to reset starting in 2010, and once those mortgage payments go up there are once again going to be millons of people who simply cannot pay their mortgages. The chart below reveals just how bad the second wave of adjustable rate mortgages is likely to be over the next several years....

#2) The Federal Housing Administration has announced plans to increase the amount of up-front cash paid by new borrowers and to require higher down payments from those with the poorest credit. The Federal Housing Administration currently backs about 30 percent of all new home loans and about 20 percent of all new home refinancing loans. Tighter standards are going to mean that less people will qualify for loans. Less qualifiers means that there will be less buyers for homes. Less buyers means that home prices are going to drop even more.

#3) It is getting really hard to find a job in the United States. A total of 6,130,000 U.S. workers had been unemployed for 27 weeks or more in December 2009. That was the most ever since the U.S. government started keeping track of this statistic in 1948. In fact, it is more than double the 2,612,000 U.S. workers who were unemployed for a similar length of time in December 2008. The reality is that once Americans lose their jobs they are increasingly finding it difficult to find new ones. Just check out the chart below....

#4) In December, there were also 929,000 "discouraged" workers who are not counted as part of the labor force because they have "given up" looking for work. That is the most since the U.S. government first started keeping track of discouraged workers in 1949. Many Americans have simply given up and are now chronically unemployed.

#5) Some areas of the U.S. are already virtually in a state of depression. The mayor of Detroit estimates that the real unemployment rate in his city is now somewhere around 50 percent.

#6) For decades, our leaders in Washington pushed us towards "a global economy" and told us it would be so good for us. But there is a flip side. Now workers in the U.S. must compete with workers all over the world, and our greedy corporations are free to pursue the cheapest labor available anywhere on the globe. Millions of jobs have already been shipped out of the United States, and Princeton University economist Alan S. Blinder estimates that 22% to 29% of all current U.S. jobs will be offshorable within two decades. The days when blue collar workers could live the American Dream are gone and they are not going to come back.

#7) During the 2001 recession, the U.S. economy lost 2% of its jobs and it took four years to get them back. This time around the U.S. economy has lost more than 5% of its jobs and there is no sign that the bleeding of jobs is going to stop any time soon.

#8) All of this unemployment is putting severe stress on state unemployment funds. At this point, 25 state unemployment insurance funds have gone broke and the Department of Labor estimates that 15 more state unemployment funds will likely go broke within two years and will need massive loans from the federal government just to keep going.

#9) 37 million Americans now receive food stamps, and the program is expanding at a pace of about 20,000 people a day. The United States of America is very quickly becoming a socialist welfare state.

#10) The number of Americans who are going broke is staggering. 1.41 million Americans filed for personal bankruptcy in 2009 - a 32 percent increase over 2008.

#11) For decades, the fact that the U.S. dollar was the reserve currency of the world gave the U.S. financial system an unusual degree of stability. But all of that is changing. Foreign countries are increasingly turning away from the dollar to other currencies. For example, Russia’s central bank announced on Wednesday that it had started buying Canadian dollars in a bid to diversify its foreign exchange reserves.

#12) The recent economic downturn has left some localities totally bankrupt. For instance, Jefferson County, Alabama is on the brink of what would be the largest government bankruptcy in the history of the United States - surpassing the 1994 filing by Southern California's Orange County.

#13) The U.S. is facing a pension crisis of unprecedented magnitude. Virtually all pension funds in the United States, both private and public, are massively underfunded. With millions of Baby Boomers getting ready to retire, there is simply no way on earth that all of these obligations can be met. Robert Novy-Marx of the University of Chicago and Joshua D. Rauh of Northwestern's Kellogg School of Management recently calculated the collective unfunded pension liability for all 50 U.S. states for Forbes magazine. So what was the total? 3.2 trillion dollars.

#14) Social Security and Medicare expenses are wildly out of control. Once again, with millions of Baby Boomers now at retirement age there is simply going to be no way to pay all of these retirees what they are owed.

#15) So will the U.S. government come to the rescue? The U.S. has allowed the total federal debt to balloon by 50% since 2006 to $12.3 trillion. The chart below is a bit outdated, but it does show the reckless expansion of U.S. government debt over the past several decades. To get an idea of where we are now, just add at least 3 trillion dollars on to the top of the chart....

#16) So has the U.S. government learned anything from these mistakes? No. In fact, Senate Democrats on Wednesday proposed allowing the federal government to borrow an additional $2 trillion to pay its bills, a record increase that would allow the U.S. national debt to reach approximately $14.3 trillion.

#17) It is going to become even harder for the U.S. government to pay the bills now that tax receipts are falling through the floor. U.S. corporate income tax receipts were down 55% in the year that ended on September 30th, 2009.

#18) So where will the U.S. government get the money? From the Federal Reserve of course. The Federal Reserve bought approximately 80 percent of all U.S. Treasury securities issued in 2009. In other words, the U.S. government is now being financed by a massive Ponzi scheme.

#19) The reckless expansion of the money supply by the U.S. government and the Federal Reserve is going to end up destroying the U.S. dollar and the value of the remaining collective net worth of all Americans. The more dollars there are, the less each individual dollar is worth. In essence, inflation is like a hidden tax on each dollar that you own. When they flood the economy with money, the value of the money you have in your bank accounts goes down. The chart below shows the growth of the U.S. money supply. Pay particular attention to the very end of the chart which shows what has been happening lately. What do you think this is going to do to the value of the U.S. dollar?....

#20) When a nation practices evil, there is no way that it is going to be blessed in the long run. The truth is that we have become a nation that is dripping with corruption and wickedness from the top to the bottom. Unless this fundamentally changes, not even the most perfect economic policies in the world are going to do us any good. In the end, you always reap what you sow. The day of reckoning for the U.S. economy is here and it is not going to be pleasant.

Monday, January 25, 2010

Your Life with Google

Google is nice. It is free software that is unobtrusive, makes life easier, and catalogues all your moves. Here is funny movie, but rings very true...

Thursday, January 21, 2010

The World Bids Farewell to Obama

US President Barack Obama suffered a painful defeat in Massachusetts on Tuesday. With mid-term elections looming, it means that Obama will have to fundamentally re-think his political course. German commentators say it is the end of hope.

US President Barack Obama suffered a painful defeat in Massachusetts on Tuesday. With mid-term elections looming, it means that Obama will have to fundamentally re-think his political course. German commentators say it is the end of hope.

US President Barack Obama has had a number of difficult weeks during his first year in the White House. Right after he took office, he had to wade through a week full of partisan bickering over his economic stimulus package combined with a tax scandal surrounding Tom Daschle, the man Obama had hoped would lead his health care reform team.

Then there was the last week of 2009, when a failed terror attack on a flight inbound for Detroit exposed major flaws in US efforts to identify and stop potential terrorists.

This week, though -- a week when Obama should have been celebrating the first anniversary of his inauguration -- may have been the president's worst yet. Scott Brown, an almost unknown Republican member of the Massachusetts Senate, defeated the Democratic candidate Martha Coakley for the US Senate seat vacated by the death of Senator Edward M. Kennedy. The defeat in a heavily Democratic state not only highlights Obama's massive loss of popular support during his first year in office, but it also could spell doom for his signature effort to reform the US health care system.

There were immediate calls for a suspension of health care votes in the Senate until Brown is sworn in. The loss of the Massachusetts seat means that the Democrats no longer control the 60 Senate seats necessary to avoid a filibuster. Obama's reform package, which aims to provide health insurance to most of the over 40 million Americans currently lacking coverage, may ultimately fail as a result.

More than that, though, the vote shows just how quickly the political pendulum has swung back to the right following Obama's election. The seat Brown won had been in Democratic hands for all but six years since 1926. Now, its new occupant is a man who not only opposes the health care bill, but also favors waterboarding as a method of interrogation for terrorism suspects and rejects carbon cap-and-trade as a means of limiting carbon emissions.

The omen could be a dark one for the Obama administration heading into a mid-term election year. German commentators take a closer look.

Center-left daily Süddeutsche Zeitung writes on Thursday:

"Obama made a serious misjudgement. Right at the beginning of his first year in office, he saved the banks, rescued the automobile industry from collapse and passed a huge economic stimulus package. He had hoped that these enormous deeds would give him the space to address those issues which are dearest to him: health care reform, climate change and investment in education."

"Those issues, however, are clearly not priorities for people in the US at the moment. Scott Brown campaigned on two promises, both of which apparently struck a nerve with the electorate. He wants to block health care reform and he wants to find ways to reduce the enormous budget deficit. It is here where the roots of dissatisfaction with Obama are to be found. His reform agenda, in its current form, is highly suspect to Americans. And they have the impression that, if he continues piling up debt, he will be gambling away the country's future."

The Financial Times Deutschland writes:

"For Obama, the election in Massachusetts means that he will have to re-evaluate his political style. He could now focus his concentration on his political base and push through his policy agenda. After all, he still has a majority in Congress -- he could back away from his strategy of bipartisanship ... which would mean giving up much of what he spent his first year in office creating."

"More likely, however, is that Obama will interpret the Massachusetts loss as a signal that he should move further toward the middle and make more concessions to the conservatives -- even if this alienates his base even further, a base which had high expectations from the 'yes we can' candidate."

"For everyone else in the world, this means that they will have to bid farewell to a candidate for whom the hopes were so high. They will have to say goodbye to the charisma they fell in love with. Obama will be staying home after all."

The left-leaning daily Die Tageszeitung writes:

"In addition to health care reform, Obama's reputation has primarily been harmed by the high unemployment rate and the increasingly unpopular war in Afghanistan. It will become even more difficult in the future for the president to push projects through successfully. Not just because Republicans now have a means of preventing it, but also because the Democratic camp is deeply divided. Some would like to see the party shift toward the center -- wherever that may be -- whereas others want the party to position itself to the left. Such a battle is hardly a good sign for the mid-term elections in November. Massachusetts could prove to be an omen."

The center-right Frankfurter Allgemeine Zeitung writes:

"Of course the president rejects the interpretation that the Massachusetts election was a referendum on his first year in the White House. But he cannot ignore the fact that his health care reform package is not popular, the situation of the country's finances is seen as threatening and many voters blame the high unemployment rate on the party in power -- on the Democrats, led by Obama. The result is a second year in office full of very different challenges than the first. To save what there is to be saved, Obama will have to be prepared to fashion a bipartisan compromise on health care -- a compromise with a Republican Party which has tasted blood and can now dream once again about a return to power."

Tuesday, January 19, 2010

Will the Feds Fund Deficits with 401(k)s?

The writing is on the wall for retirement assets held in conventional ways. A report last week in Business Week shows that the U.S. Feds have 401(k) assets in their sites.

The writing is on the wall for retirement assets held in conventional ways. A report last week in Business Week shows that the U.S. Feds have 401(k) assets in their sites.“The U.S. Treasury and Labor Departments will ask for public comment as soon as next week on ways to promote the conversion of 401(k) savings and Individual Retirement Accounts into annuities or other steady payment streams, according to Assistant Labor Secretary Phyllis C. Borzi and Deputy Assistant Treasury Secretary Mark Iwry, who are spearheading the effort."

“Annuities generally guarantee income until the retiree’s death, and often that of a surviving spouse as well. They are designed to protect against the risk that retirees outlive their savings, a danger made clear by market losses suffered by older Americans over the last year, David Certner, legislative counsel for AARP, said in an interview.”

Now ostensibly, the plan to offer an annuity option for 401(k) plans will seem sensible. But don’t be fooled.

This is the beginning of a money grab by the Feds for the $3.6 trillion in assets held by U.S. 401(k)s. The Feds need that money to finance the deficit. This is where some of the money to fund the deficits may come from, answering a question we asked earlier in the week. What you can’t take, you’ll have to print.

But right now, the Feds can’t just take that 401(k) money. Well, they could. But it would crash stocks and infuriate the public, leading to some civic violence. What’s more, it would feel like theft as well as looking (and being) like it. So they have to dress the plan up as something that’s better for savers.

They’re trotting out the idea that a defined benefit pension plan is better than defined contribution plan (which is true, if it’s funded well). A defined benefit plan guarantees you income in your old age years. A defined contribution plan (what we have now) just guarantees money flows into the stock market (which is good for the financial services industry, but don’t guarantee you’ll have any money when you really need it later in life).

The U.S. Treasury Department and the Obama administration are exploring ways to encourage U.S. savers to buy more annuities or investment vehicles composed of “safe” assets. What constitutes safe? Why 30-year U.S. government bonds of course! Thus, the government can encourage people to buy what the Chinese and the Japanese and most other U.S. creditors don’t want to touch any longer.

The trouble with an annuity or 30-year bond is that you get crushed by inflation. In principle, it’s not different that a zero coupon bond. You get your nominal investment back upon redemption. But you are not compensated for inflation and your money is tied up, instead of working harder for you elsewhere.

It’s obvious what the Fed’s get out of this: a ready source of new funds to buy their bonds. This kicks the can of unsustainable deficit spending down the road a few months, or perhaps a few years. But it doesn’t change the fundamentally destructive path of U.S. fiscal policy.

What it does tell you is that mischief is afoot among the wealth stealers of the modern nation state? Faced with a failed funding model, they are beginning their cash grab. This takes the form of higher taxes. But the big bounty is the retirement savings of millions of Americans.

This solves the problem of having to sell the debt to foreign investors. And it solves the problem of having to make tough budget deficits. Just issue more debt and make the super funds buy it with your money.

If you think that’s balderdash or won’t happen, you’re being naïve. It won’t happen overnight. But it will happen gradually. It’s evolving towards that already. If they can’t get it through tax or royalty revenues, the tax posse will get it by any means necessary, which means your super assets are an obvious target.

Alarmist? Irresponsible? You decide. But we can see the evolution of this as clear as day, even if saying it in public is bad form or taboo. But now is the time to say the taboo things.

Dan Denning Article

Monday, January 18, 2010

One in 7 U.S. mortgages foreclosing or delinquent

NEW YORK, Nov 19 (Reuters) - A record one in seven U.S. mortgages were in foreclosure or at least one payment past due in the third quarter, according to fresh data signaling the recovery in the housing market will be tepid at best.

U.S. mortgage delinquency rates and the percentage of loans that entered the foreclosure process also jumped to records from July to September, the Mortgage Bankers Association said on Thursday.

Rising job losses were behind the increasingly bleak portrait of the housing market in a trend that will continue into next year, the group said in data that adds to recent evidence of a still-struggling housing market.

Housing and related business account for about 20 percent of the economy and recovery is essential to bring unemployment down from a 26-1/2-year high and kick-start economic growth.

Yet record foreclosures will add to the growing supply of unsold homes, sapping the housing market as it attempts to recover from the worst slump since the Great Depression.

The MBA said the percentage of loans in foreclosure rose to 1.42 percent, from 1.36 percent in the second quarter and 1.07 percent in the third quarter of 2008.

"Foreclosures remain the biggest hurdle to the housing recovery," said Michelle Meyer, economist at Barclays Capital in New York.

"Foreclosures will be worse in the first part of 2010 and we do not see a peak in foreclosures until the middle of next year."

More conservative, prime fixed-rate loans often sold to homebuyers with the highest credit ratings continued to represent the largest share of foreclosures started and were the biggest driver of the increase in foreclosures, said MBA chief economist Jay Brinkmann.

The delinquency rate for mortgage loans on one-to-four-unit residential properties rose to a seasonally adjusted rate of 9.64 percent of loans outstanding, up from 9.24 percent in the second quarter and 6.99 percent a year earlier, the MBA said.

The delinquency rate broke the record set last quarter, based on MBA data going back to 1972. The rate includes loans that are at least one payment past due but does not include loans somewhere in the process of foreclosure.

The latest splash of cold water follows a stunning 10.6 percent plunge in housing starts for October, reported on Wednesday. For details see [ID:nN1899353].

The combination of loans in foreclosure and at least one payment past due was 14.41 percent on a non-seasonally adjusted basis, the highest ever seen in the survey.

In fact, 33 percent of foreclosures started in the third quarter were on prime fixed-rate loans and those loans were 44 percent of the quarterly increase in foreclosures, Brinkmann said.

"The foreclosure numbers for prime fixed-rate loans will get worse because those loans represented 54 percent of the quarterly increase in loans 90 days or more past due but not yet in foreclosure," he said.

The percentage of loans in the foreclosure process at the end of the third quarter was 4.47 percent, up from 4.30 percent in the second quarter and 2.97 percent a year earlier.

Florida, California, Arizona and Nevada have a disproportionate share of these problems, Brinkmann said.

They had 43 percent of all foreclosures started in the third quarter, down from 44 percent both last quarter and the third quarter last year. They had 37 percent of the nation's prime fixed-rate loan foreclosure starts and 67 percent of the prime adjustable-rate mortgage, or ARM, foreclosure starts.

At the end of September, 25 percent of mortgages in Florida were at least one payment past due or in foreclosure, he said.

OUTLOOK BLEAK

The outlook is for delinquency and foreclosure rates to continue to worsen before they improve, Brinkmann said.

"First, it is unlikely the employment picture will get better until sometime next year and even then jobs will increase at a very slow pace," he said.

"Second, the number of loans 90 days or more past due or in foreclosure is now a little over 4 million as compared with 3.9 million new and previously occupied homes currently for sale, although there is likely some overlap between the two numbers," he said.

Therefore, the ultimate resolution of these seriously delinquent loans will put added pressure on the hardest hit sections of the country, Brinkmann said.

Reuters

U.S. mortgage delinquency rates and the percentage of loans that entered the foreclosure process also jumped to records from July to September, the Mortgage Bankers Association said on Thursday.

Rising job losses were behind the increasingly bleak portrait of the housing market in a trend that will continue into next year, the group said in data that adds to recent evidence of a still-struggling housing market.

Housing and related business account for about 20 percent of the economy and recovery is essential to bring unemployment down from a 26-1/2-year high and kick-start economic growth.

Yet record foreclosures will add to the growing supply of unsold homes, sapping the housing market as it attempts to recover from the worst slump since the Great Depression.

The MBA said the percentage of loans in foreclosure rose to 1.42 percent, from 1.36 percent in the second quarter and 1.07 percent in the third quarter of 2008.

"Foreclosures remain the biggest hurdle to the housing recovery," said Michelle Meyer, economist at Barclays Capital in New York.

"Foreclosures will be worse in the first part of 2010 and we do not see a peak in foreclosures until the middle of next year."

More conservative, prime fixed-rate loans often sold to homebuyers with the highest credit ratings continued to represent the largest share of foreclosures started and were the biggest driver of the increase in foreclosures, said MBA chief economist Jay Brinkmann.

The delinquency rate for mortgage loans on one-to-four-unit residential properties rose to a seasonally adjusted rate of 9.64 percent of loans outstanding, up from 9.24 percent in the second quarter and 6.99 percent a year earlier, the MBA said.

The delinquency rate broke the record set last quarter, based on MBA data going back to 1972. The rate includes loans that are at least one payment past due but does not include loans somewhere in the process of foreclosure.

The latest splash of cold water follows a stunning 10.6 percent plunge in housing starts for October, reported on Wednesday. For details see [ID:nN1899353].

The combination of loans in foreclosure and at least one payment past due was 14.41 percent on a non-seasonally adjusted basis, the highest ever seen in the survey.

In fact, 33 percent of foreclosures started in the third quarter were on prime fixed-rate loans and those loans were 44 percent of the quarterly increase in foreclosures, Brinkmann said.

"The foreclosure numbers for prime fixed-rate loans will get worse because those loans represented 54 percent of the quarterly increase in loans 90 days or more past due but not yet in foreclosure," he said.

The percentage of loans in the foreclosure process at the end of the third quarter was 4.47 percent, up from 4.30 percent in the second quarter and 2.97 percent a year earlier.

Florida, California, Arizona and Nevada have a disproportionate share of these problems, Brinkmann said.

They had 43 percent of all foreclosures started in the third quarter, down from 44 percent both last quarter and the third quarter last year. They had 37 percent of the nation's prime fixed-rate loan foreclosure starts and 67 percent of the prime adjustable-rate mortgage, or ARM, foreclosure starts.

At the end of September, 25 percent of mortgages in Florida were at least one payment past due or in foreclosure, he said.

OUTLOOK BLEAK

The outlook is for delinquency and foreclosure rates to continue to worsen before they improve, Brinkmann said.

"First, it is unlikely the employment picture will get better until sometime next year and even then jobs will increase at a very slow pace," he said.

"Second, the number of loans 90 days or more past due or in foreclosure is now a little over 4 million as compared with 3.9 million new and previously occupied homes currently for sale, although there is likely some overlap between the two numbers," he said.

Therefore, the ultimate resolution of these seriously delinquent loans will put added pressure on the hardest hit sections of the country, Brinkmann said.

Reuters

Friday, January 15, 2010

The NBA or NFL

Even if you aren't a sports fan this is very interesting!

? ? ? ? ? ? ? ? ?

36 have been accused of spousal abuse

7 have been arrested for fraud

19 have been accused of writing bad checks

117 have directly or indirectlybankrupted at least 2 businesses

3 have done time for assault

71repeat71

cannot get a credit card due to bad credit

14 have been arrested on drug-related charges

8 have been arrested for shoplifting

21currently are defendants in lawsuits,

and

84have been arrested for drunk driving

in the last year

Can

you guess which organization this is?

NBA Or NFL

?

Give up yet?

Neither,

it's the 535 members of the

United States Congress

The same group of Idiots that crank out

hundreds of new laws each year

designed to keep the rest of us in line.

? ? ? ? ? ? ? ? ?

36 have been accused of spousal abuse

7 have been arrested for fraud

19 have been accused of writing bad checks

117 have directly or indirectlybankrupted at least 2 businesses

3 have done time for assault

71repeat71

cannot get a credit card due to bad credit

14 have been arrested on drug-related charges

8 have been arrested for shoplifting

21currently are defendants in lawsuits,

and

84have been arrested for drunk driving

in the last year

Can

you guess which organization this is?

NBA Or NFL

?

Give up yet?

Neither,

it's the 535 members of the

United States Congress

The same group of Idiots that crank out

hundreds of new laws each year

designed to keep the rest of us in line.

Thursday, January 14, 2010

Wednesday, January 13, 2010

The Truth About the Health Care Bills

The Truth About the Health Care Bills - Michael Connelly, Ret. Constitutional Attorney

Well, I have done it! I have read the entire text of proposed House Bill 3200: The Affordable Health Care Choices Act of 2009. I studied it with particular emphasis from my area of expertise, constitutional law. I was frankly concerned that parts of the proposed law that were being discussed might be unconstitutional. What I found was far worse than what I had heard or expected.

To begin with, much of what has been said about the law and its implications is in fact true, despite what the Democrats and the media are saying. The law does provide for rationing of health care, particularly where senior citizens and other classes of citizens are involved, free health care for illegal immigrants, free abortion services, and probably forced participation in abortions by members of the medical profession.

The Bill will also eventually force private insurance companies out of business, and put everyone into a government run system. All decisions about personal health care will ultimately be made by federal bureaucrats, and most of them will not be health care professionals. Hospital admissions, payments to physicians, and allocations of necessary medical devices will be strictly controlled by the government.

However, as scary as all of that is, it just scratches the surface. In fact, I have concluded that this legislation really has no intention of providing affordable health care choices. Instead it is a convenient cover for the most massive transfer of power to the Executive Branch of government that has ever occurred, or even been contemplated If this law or a similar one is adopted, major portions of the Constitution of the United States will effectively have been destroyed.

The first thing to go will be the masterfully crafted balance of power between the Executive, Legislative, and Judicial branches of the U.S. Government. The Congress will be transferring to the Obama Administration authority in a number of different areas over the lives of the American people, and the businesses they own.

The irony is that the Congress doesn't have any authority to legislate in most of those areas to begin with! I defy anyone to read the text of the U.S. Constitution and find any authority granted to the members of Congress to regulate health care.

This legislation also provides for access, by the appointees of the Obama administration, of all of your personal healthcare direct violation of the specific provisions of the 4th Amendment to the Constitution information, your personal financial information, and the information of your employer, physician, and hospital. All of this is a protecting against unreasonable searches and seizures. You can also forget about the right to privacy. That will have been legislated into oblivion regardless of what the 3rd and 4th Amendments may provide.

If you decide not to have healthcare insurance, or if you have private insurance that is not deemed acceptable to the Health Choices Administrator appointed by Obama, there will be a tax imposed on you. It is called a tax instead of a fine because of the intent to avoid application of the due process clause of the 5th Amendment. However, that doesn't work because since there is nothing in the law that allows you to contest or appeal the imposition of the tax, it is definitely depriving someone of property without the due process of law.

So, there are three of those pesky amendments that the far left hate so much, out the original ten in the Bill of Rights, that are effectively nullified by this law. It doesn't stop there though.

The 9th Amendment that provides: The enumeration in the Constitution, of certain rights, shall not be construed to deny or disparage others retained by the people;

The 10th Amendment states: The powers not delegated to the United States by the Constitution, nor prohibited by it to the States, are preserved to the States respectively, or to the people. Under the provisions of this piece of Congressional handiwork neither the people nor the states are going to have any rights or powers at all in many areas that once were theirs to control.

I could write many more pages about this legislation, but I think you get the idea. This is not about health care; it is about seizing power and limiting rights. Article 6 of the Constitution requires the members of both houses of Congress to "be bound by oath or affirmation to support the Constitution." If I was a member of Congress I would not be able to vote for this legislation or anything like it, without feeling I was violating that sacred oath or affirmation. If I voted for it anyway, I would hope the American people would hold me accountable.

For those who might doubt the nature of this threat, I suggest they consult the source, the US Constitution, and Bill of Rights. There you can see exactly what we are about to have taken from us.

Michael Connelly

Retired attorney,

Constitutional Law Instructor

Carrollton , Texas

Well, I have done it! I have read the entire text of proposed House Bill 3200: The Affordable Health Care Choices Act of 2009. I studied it with particular emphasis from my area of expertise, constitutional law. I was frankly concerned that parts of the proposed law that were being discussed might be unconstitutional. What I found was far worse than what I had heard or expected.

To begin with, much of what has been said about the law and its implications is in fact true, despite what the Democrats and the media are saying. The law does provide for rationing of health care, particularly where senior citizens and other classes of citizens are involved, free health care for illegal immigrants, free abortion services, and probably forced participation in abortions by members of the medical profession.

The Bill will also eventually force private insurance companies out of business, and put everyone into a government run system. All decisions about personal health care will ultimately be made by federal bureaucrats, and most of them will not be health care professionals. Hospital admissions, payments to physicians, and allocations of necessary medical devices will be strictly controlled by the government.

However, as scary as all of that is, it just scratches the surface. In fact, I have concluded that this legislation really has no intention of providing affordable health care choices. Instead it is a convenient cover for the most massive transfer of power to the Executive Branch of government that has ever occurred, or even been contemplated If this law or a similar one is adopted, major portions of the Constitution of the United States will effectively have been destroyed.

The first thing to go will be the masterfully crafted balance of power between the Executive, Legislative, and Judicial branches of the U.S. Government. The Congress will be transferring to the Obama Administration authority in a number of different areas over the lives of the American people, and the businesses they own.

The irony is that the Congress doesn't have any authority to legislate in most of those areas to begin with! I defy anyone to read the text of the U.S. Constitution and find any authority granted to the members of Congress to regulate health care.

This legislation also provides for access, by the appointees of the Obama administration, of all of your personal healthcare direct violation of the specific provisions of the 4th Amendment to the Constitution information, your personal financial information, and the information of your employer, physician, and hospital. All of this is a protecting against unreasonable searches and seizures. You can also forget about the right to privacy. That will have been legislated into oblivion regardless of what the 3rd and 4th Amendments may provide.

If you decide not to have healthcare insurance, or if you have private insurance that is not deemed acceptable to the Health Choices Administrator appointed by Obama, there will be a tax imposed on you. It is called a tax instead of a fine because of the intent to avoid application of the due process clause of the 5th Amendment. However, that doesn't work because since there is nothing in the law that allows you to contest or appeal the imposition of the tax, it is definitely depriving someone of property without the due process of law.

So, there are three of those pesky amendments that the far left hate so much, out the original ten in the Bill of Rights, that are effectively nullified by this law. It doesn't stop there though.

The 9th Amendment that provides: The enumeration in the Constitution, of certain rights, shall not be construed to deny or disparage others retained by the people;

The 10th Amendment states: The powers not delegated to the United States by the Constitution, nor prohibited by it to the States, are preserved to the States respectively, or to the people. Under the provisions of this piece of Congressional handiwork neither the people nor the states are going to have any rights or powers at all in many areas that once were theirs to control.

I could write many more pages about this legislation, but I think you get the idea. This is not about health care; it is about seizing power and limiting rights. Article 6 of the Constitution requires the members of both houses of Congress to "be bound by oath or affirmation to support the Constitution." If I was a member of Congress I would not be able to vote for this legislation or anything like it, without feeling I was violating that sacred oath or affirmation. If I voted for it anyway, I would hope the American people would hold me accountable.

For those who might doubt the nature of this threat, I suggest they consult the source, the US Constitution, and Bill of Rights. There you can see exactly what we are about to have taken from us.

Michael Connelly

Retired attorney,

Constitutional Law Instructor

Carrollton , Texas

Tuesday, January 12, 2010

SEC order helps maintain AIG bailout mystery

* SEC agreed with AIG to keep some bailout terms sealed

NEW YORK, Jan 11 (Reuters) - It could take until November 2018 to get the full story behind the U.S. bailout of insurance giant American International Group (AIG.N) because of an action taken last year by the Securities and Exchange Commission.

In May, the SEC approved a request by AIG to keep secret an exhibit to a year-old regulatory filing that includes some of the details on the most controversial aspect of the AIG bailout: the funneling of tens of billions of dollars to big banks like Societe Generale, Goldman Sachs (GS.N), Deutsche Bank (DBKGn.DE) and Merrill Lynch.

The SEC's Division of Corporation Finance, in granting AIG's request for confidential treatment, said the "excluded information" will not be made public until Nov. 25, 2018, according to a copy of the agency's May 22 order.

The SEC said the insurer had demonstrated the information in the exhibit, called Schedule A, "qualifies as confidential commercial or financial information."

The expiration date for the SEC order falls on the 10th anniversary of Federal Reserve of New York's decision to provide emergency financing to an entity set up to specifically acquire some $60 billion in collateralized debt obligations from 16 banks in the United States and Europe.

All the banks that got money from the Fed-sponsored entity -- Maiden Lane III -- had purchased insurance contracts, or credit default swaps, on those mortgage-related securities from AIG.

The SEC's decision to approve AIG's request for confidential treatment got scant attention at the time. But it could spark controversy now following the release last week of 14-month-old emails that reveal that some at the New York Fed had discussions with AIG officials about how much information should be disclosed to the public about the Maiden Lane III transaction.

The New York Fed, then led by Treasury Secretary Timothy Geithner, plays a critical role in the world of finance given its close dealings with all the major Wall Street banks, many of which were counterparties of AIG.

SEC spokesman John Nestor declined to comment on the reasons for granting AIG's request to treat the exhibit as confidential.

In a typical year, the SEC receives 1,500 requests from U.S. companies for confidential treatment for portions of regulatory filing, said Nestor. The agency grants those requests, "all or in part," 95 percent of the time, he said.

It's not clear what information is in the exhibit beyond a listing of the 16 banks that were beneficiaries of the Maiden Lane transaction. Last March, under pressure from Congress, AIG released the names of the banks that sold CDOs to Maiden Lane and how much money the banks got in the process.

When AIG filed the Schedule A exhibit with the SEC, it redacted the information it wanted to keep confidential, in anticipation regulators would approve its request.

The Fed's bailout of AIG long has been controversial because the banks that sold CDOs to Maiden Lane III were paid 100 percent of face value, even though many of the securities were worth substantially less at the time of the government bailout.

Last Thursday the furor over the Maiden Lane transaction was reignited after Rep. Darrell Issa, a California Republican, released copies of emails detailing discussions between the New York Fed and AIG over how much information to disclose.

The emails have provided fresh ammunition for critics of Geithner. New York Fed General Counsel Thomas Baxter Jr. said in a letter to Issa's office that Geithner "played no role in, and had no knowledge of" the emails.

Issa, the highest-ranking Republican on the House Committee on Oversight and Government Reform, said the panel will soon hold hearings about how information was disclosed to the public about the Maiden Lane deal.

Issa's spokesman Kurt Bardella declined to comment on the SEC's handling of the AIG's confidentiality request.

But Issa, in a prepared statement, said "as much information as possible should be made available to Congress to review the details and decisions" regarding the payments.

The batch of emails released by Issa discussed the SEC's requests for more information about the exhibit that AIG wanted to keep secret. But the emails did not mention the SEC's decision to grant AIG's request for confidential treatment.

NEW YORK, Jan 11 (Reuters) - It could take until November 2018 to get the full story behind the U.S. bailout of insurance giant American International Group (AIG.N) because of an action taken last year by the Securities and Exchange Commission.

In May, the SEC approved a request by AIG to keep secret an exhibit to a year-old regulatory filing that includes some of the details on the most controversial aspect of the AIG bailout: the funneling of tens of billions of dollars to big banks like Societe Generale, Goldman Sachs (GS.N), Deutsche Bank (DBKGn.DE) and Merrill Lynch.

The SEC's Division of Corporation Finance, in granting AIG's request for confidential treatment, said the "excluded information" will not be made public until Nov. 25, 2018, according to a copy of the agency's May 22 order.

The SEC said the insurer had demonstrated the information in the exhibit, called Schedule A, "qualifies as confidential commercial or financial information."

The expiration date for the SEC order falls on the 10th anniversary of Federal Reserve of New York's decision to provide emergency financing to an entity set up to specifically acquire some $60 billion in collateralized debt obligations from 16 banks in the United States and Europe.

All the banks that got money from the Fed-sponsored entity -- Maiden Lane III -- had purchased insurance contracts, or credit default swaps, on those mortgage-related securities from AIG.

The SEC's decision to approve AIG's request for confidential treatment got scant attention at the time. But it could spark controversy now following the release last week of 14-month-old emails that reveal that some at the New York Fed had discussions with AIG officials about how much information should be disclosed to the public about the Maiden Lane III transaction.

The New York Fed, then led by Treasury Secretary Timothy Geithner, plays a critical role in the world of finance given its close dealings with all the major Wall Street banks, many of which were counterparties of AIG.

SEC spokesman John Nestor declined to comment on the reasons for granting AIG's request to treat the exhibit as confidential.

In a typical year, the SEC receives 1,500 requests from U.S. companies for confidential treatment for portions of regulatory filing, said Nestor. The agency grants those requests, "all or in part," 95 percent of the time, he said.

It's not clear what information is in the exhibit beyond a listing of the 16 banks that were beneficiaries of the Maiden Lane transaction. Last March, under pressure from Congress, AIG released the names of the banks that sold CDOs to Maiden Lane and how much money the banks got in the process.

When AIG filed the Schedule A exhibit with the SEC, it redacted the information it wanted to keep confidential, in anticipation regulators would approve its request.

The Fed's bailout of AIG long has been controversial because the banks that sold CDOs to Maiden Lane III were paid 100 percent of face value, even though many of the securities were worth substantially less at the time of the government bailout.

Last Thursday the furor over the Maiden Lane transaction was reignited after Rep. Darrell Issa, a California Republican, released copies of emails detailing discussions between the New York Fed and AIG over how much information to disclose.

The emails have provided fresh ammunition for critics of Geithner. New York Fed General Counsel Thomas Baxter Jr. said in a letter to Issa's office that Geithner "played no role in, and had no knowledge of" the emails.

Issa, the highest-ranking Republican on the House Committee on Oversight and Government Reform, said the panel will soon hold hearings about how information was disclosed to the public about the Maiden Lane deal.

Issa's spokesman Kurt Bardella declined to comment on the SEC's handling of the AIG's confidentiality request.

But Issa, in a prepared statement, said "as much information as possible should be made available to Congress to review the details and decisions" regarding the payments.

The batch of emails released by Issa discussed the SEC's requests for more information about the exhibit that AIG wanted to keep secret. But the emails did not mention the SEC's decision to grant AIG's request for confidential treatment.

Thursday, January 7, 2010

Geithner’s Fed Told AIG to Limit Swaps Disclosure

Was reading Bloomberg today and came across a very interesting Story, which is kind of HUGE !!

Was reading Bloomberg today and came across a very interesting Story, which is kind of HUGE !!Story on Bloomberg.com

The Federal Reserve Bank of New York, then led by Timothy Geithner, told American International Group Inc. to withhold details from the public about the bailed-out insurer’s payments to banks during the depths of the financial crisis, e-mails between the company and its regulator show.

AIG said in a draft of a regulatory filing that the insurer paid banks, which included Goldman Sachs Group Inc. and Societe Generale SA, 100 cents on the dollar for credit-default swaps they bought from the firm. The New York Fed crossed out the reference, according to the e-mails, and AIG excluded the language when the filing was made public on Dec. 24, 2008. The e-mails were obtained by Representative Darrell Issa, ranking member of the House Oversight and Government Reform Committee.

The New York Fed took over negotiations between AIG and the banks in November 2008 as losses on the swaps, which were contracts tied to subprime home loans, threatened to swamp the insurer weeks after its taxpayer-funded rescue. The regulator decided that Goldman Sachs and more than a dozen banks would be fully repaid for $62.1 billion of the swaps, prompting lawmakers to call the AIG rescue a “backdoor bailout” of financial firms.

“It appears that the New York Fed deliberately pressured AIG to restrict and delay the disclosure of important information,” said Issa, a California Republican. Taxpayers “deserve full and complete disclosure under our nation’s securities laws, not the withholding of politically inconvenient information.” President Barack Obama selected Geithner as Treasury secretary, a post he took last year.

Bank Payments

Issa requested the e-mails from AIG Chief Executive Officer Robert Benmosche in October after Bloomberg News reported that the New York Fed ordered the crippled insurer not to negotiate for discounts in settling the swaps. The decision to pay the banks in full may have cost AIG, and thus taxpayers, at least $13 billion, based on the discount the insurer was seeking.

The e-mail exchanges between AIG and the New York Fed over the insurer’s disclosure of the transactions show that the regulator pressed the company to keep details out of the public eye. Issa’s comments add to criticism from Republican lawmakers, including Senator Chuck Grassley of Iowa and Representative Roy Blunt of Missouri, who wrote letters in the past two months demanding information from Geithner, 48, about the costs of the AIG bailout.

Securities Lawyers

AIG’s Dec. 24, 2008, filing was challenged privately by the U.S. Securities and Exchange Commission, which polices the adequacy of disclosures by publicly traded firms. The agency said in a letter to then-CEO Edward Liddy six days later that AIG should provide a Schedule A, which lists collateral postings for the swaps and names the bank counterparties that purchased them from the company. The Schedule A was disclosed about five months later in a filing.

“Our position has always been that if AIG’s securities lawyers determine that AIG is legally obligated to make a particular filing or disclosure, then that is what AIG must do,” said Jack Gutt, a spokesman for the New York Fed, in an e- mailed statement. Gutt said it was appropriate for the New York Fed, as party to deals outlined in the filings, “to provide comments on a number of issues, including disclosures, with the understanding that the final decision rested with AIG’s securities counsel.”

Mark Herr, a spokesman for New York-based AIG, declined to comment. Andrew Williams of the Treasury referred questions to the New York Fed.

Kathleen Shannon, an AIG deputy general counsel, wrote to the insurer’s executives in a March 12, 2009, e-mail about the conflicting demands from the New York Fed and SEC.

‘Reasonable Basis’

“In order to make only the disclosure that the Fed wants us to make,” Shannon wrote, “we need to have a reasonable basis for believing and arguing to the SEC that the information we are seeking to protect is not already publicly available.”

AIG disclosed the names of the counterparties, which included Deutsche Bank AG and Merrill Lynch & Co., on March 15. The disclosure said AIG made more than $27 billion in payments without identifying the securities tied to the swaps or listing the value of individual purchases by each bank, details the Fed wanted to keep out, according to the March 12 e-mail from AIG’s Shannon.

Earlier that month, Fed Vice Chairman Donald Kohn testified to Congress that disclosure of the counterparties would harm AIG’s ability to do business. The insurer agreed to turn over a stake of almost 80 percent in connection to its bailout.

‘No Mention of the Synthetics’

The e-mails span five months starting in November 2008 and include requests from the New York Fed to withhold documents and delay disclosures. The correspondence includes e-mails between AIG’s Shannon and attorneys at the New York Fed and its law firm, Davis Polk & Wardwell LLP. Tom Orewyler, a spokesman for Davis Polk in New York, declined to comment as did Shannon.

According to Shannon’s e-mails obtained by Issa, the New York Fed suggested that AIG refrain in a filing from mentioning so-called synthetic collateralized debt obligations, which bundled derivative contracts rather than actual loans.

The filing “reflects your client’s desire that there be no mention of the synthetics in connection with this transaction,” Shannon wrote to Davis Polk on Dec. 2, 2008. “They will not be mentioned at all.”

AIG had about $9.8 billion of swaps protecting the synthetic holdings as of September 2008, the company said on Dec. 10, 2008. Goldman Sachs said in a press release last month that it was among banks that had losses on synthetic CDOs.

As part of a bailout that swelled to $182.3 billion, AIG and the Fed created Maiden Lane III, a taxpayer-funded facility designed to remove mortgage-linked swaps from the insurer’s books. Shannon told the New York Fed on Nov. 24, 2008, that AIG executives wanted to publicly disclose details about Maiden Lane the next day.

‘Guided by Your Counsel’

“Do you think it might be feasible to hold off on the Maiden Lane III 8K and press release until next week?” Brett Phillips, a New York Fed lawyer wrote in an e-mail that day. “The thinking is that the Maiden Lane III closing will be a less transparent event, and it might be better to narrow the gap between AIG’s announcement and the New York Fed’s publication of term sheet summaries.”

“Given the significance of the transaction, AIG would be best served by filing tomorrow,” Shannon wrote. “We will of course be guided by your counsel.” The document outlining the Maiden Lane agreement was posted on Dec. 2, 2008.

In at least one instance, AIG pushed for documents to be disclosed and then released the information.

‘Better Disclosure’

“We believe that the agreements listed in the index (i.e., the Master Investment and Credit Agreement and the Shortfall Agreement) do not need to be filed,” Peter Bazos, a Davis Polk lawyer wrote on Nov. 25, 2008. “Please let us know your thoughts in this regard.”

AIG’s Shannon replied that “the better practice and better disclosure in this complex area is to file the agreements currently rather than to delay.” The agreements were included in the Dec. 2 filing.

More details of the negotiations over swaps payments emerged in November 2009 when Neil Barofsky, the special inspector in charge of policing the Troubled Asset Relief Program, assessed the Fed’s role in the bailout.

“Federal Reserve officials provided AIG’s counterparties with tens of billions of dollars they likely would have not otherwise received,” Barofsky wrote in a Nov. 17 report. “The default position, whenever government funds are deployed in a crisis to support markets or institutions, should be that the public is entitled to know what is being done with government funds.”

AIG’s first rescue was an $85 billion credit line from the New York Fed in September 2008. The bailout was expanded three times and is valued at $182.3 billion. That includes a $60 billion Fed credit line, an investment of as much as $69.8 billion from the Treasury and up to $52.5 billion for Maiden Lane facilities to buy mortgage-linked assets owned or backed by the company.

Wednesday, January 6, 2010

Window cleaning chemical injected into fast food hamburger meat

If you're in the beef business, what do you do with all the extra cow parts and trimmings that have traditionally been sold off for use in pet food? You scrape them together into a pink mass, inject them with a chemical to kill the e.coli, and sell them to fast food restaurants to make into hamburgers.

If you're in the beef business, what do you do with all the extra cow parts and trimmings that have traditionally been sold off for use in pet food? You scrape them together into a pink mass, inject them with a chemical to kill the e.coli, and sell them to fast food restaurants to make into hamburgers.That's what's been happening all across the USA with beef sold to McDonald's, Burger King, school lunches and other fast food restaurants, according to a New York Times article. The beef is injected with ammonia, a chemical commonly used in glass cleaning and window cleaning products.

This is all fine with the USDA, which endorses the procedure as a way to make the hamburger beef "safe" enough to eat. Ammonia kills e.coli, you see, and the USDA doesn't seem to be concerned with the fact that people are eating ammonia in their hamburgers.

This ammonia-injected beef comes from a company called Beef Products, Inc. As NYT reports, the federal school lunch program used a whopping 5.5 million pounds of ammonia-injected beef trimmings from this company in 2008. This company reportedly developed the idea of using ammonia to sterilize beef before selling it for human consumption.

Aside from the fact that there's ammonia in the hamburger meat, there's another problem with this company's products: The ammonia doesn't always kill the pathogens. Both e.coli and salmonella have been found contaminating the cow-derived products sold by this company.

This came as a shock to the USDA, which had actually exempted the company's products from pathogen testing and product recalls. Why was it exempted? Because the ammonia injection process was deemed so effective that the meat products were thought to be safe beyond any question.

What else is in there?